Introduction

Technology has brought with it various changes in the world of business today. With the ever-changing nature of the business environment, organizations too are adjusting some aspects of their business operations to suit the external environment. Nearly all organizations must keep up with what is new in the technology world if they are to survive in the economy. With technology, various aspects of the business organization become outdated as many companies prefer the use of technology for its availability and ease of application. From an economic point of view, the use of technology has affected the economy in different ways. Technology can be said to be the main reason behind certain phenomena of the economy. In most cases, companies have to change their business models to suit the requirements of the economy. Technology disrupts the market equilibrium by causing a shift in both demand and supply as well the general welfare of the economy needs to be adjusted to cope with the increasing demand for technology.

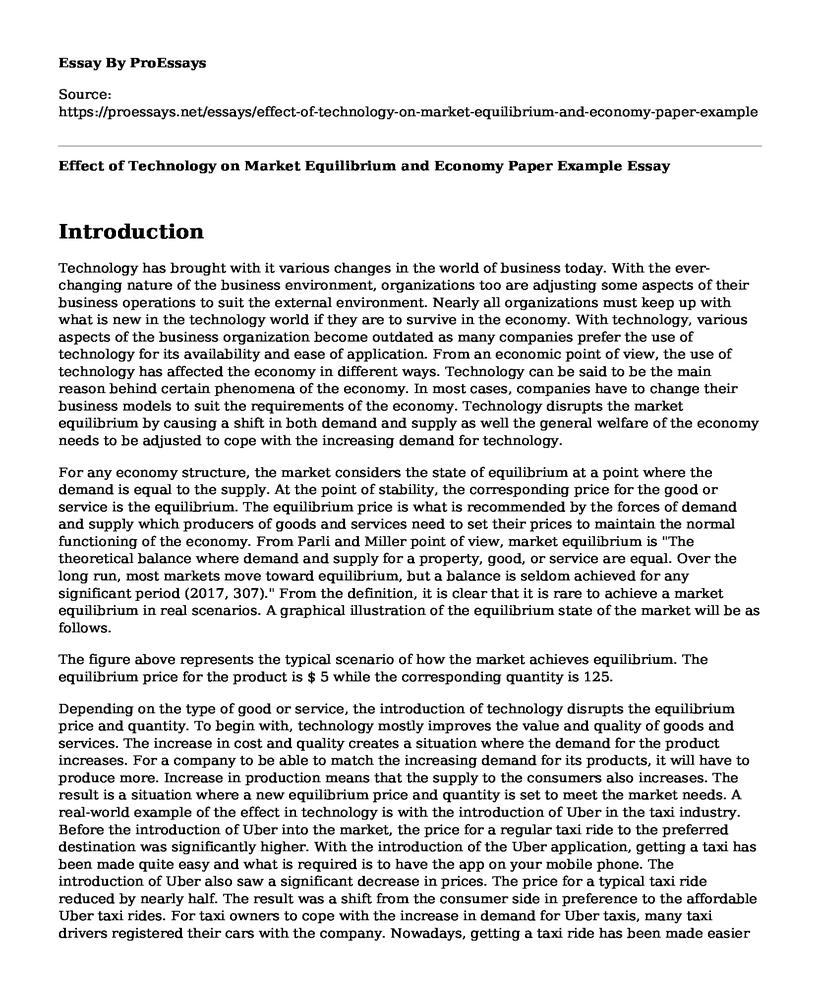

For any economy structure, the market considers the state of equilibrium at a point where the demand is equal to the supply. At the point of stability, the corresponding price for the good or service is the equilibrium. The equilibrium price is what is recommended by the forces of demand and supply which producers of goods and services need to set their prices to maintain the normal functioning of the economy. From Parli and Miller point of view, market equilibrium is "The theoretical balance where demand and supply for a property, good, or service are equal. Over the long run, most markets move toward equilibrium, but a balance is seldom achieved for any significant period (2017, 307)." From the definition, it is clear that it is rare to achieve a market equilibrium in real scenarios. A graphical illustration of the equilibrium state of the market will be as follows.

The figure above represents the typical scenario of how the market achieves equilibrium. The equilibrium price for the product is $ 5 while the corresponding quantity is 125.

Depending on the type of good or service, the introduction of technology disrupts the equilibrium price and quantity. To begin with, technology mostly improves the value and quality of goods and services. The increase in cost and quality creates a situation where the demand for the product increases. For a company to be able to match the increasing demand for its products, it will have to produce more. Increase in production means that the supply to the consumers also increases. The result is a situation where a new equilibrium price and quantity is set to meet the market needs. A real-world example of the effect in technology is with the introduction of Uber in the taxi industry. Before the introduction of Uber into the market, the price for a regular taxi ride to the preferred destination was significantly higher. With the introduction of the Uber application, getting a taxi has been made quite easy and what is required is to have the app on your mobile phone. The introduction of Uber also saw a significant decrease in prices. The price for a typical taxi ride reduced by nearly half. The result was a shift from the consumer side in preference to the affordable Uber taxi rides. For taxi owners to cope with the increase in demand for Uber taxis, many taxi drivers registered their cars with the company. Nowadays, getting a taxi ride has been made easier and cheaper than before.

The shift in demand and supply can explain the change in equilibrium as a result of technology. Shift in demand or supply in different from a change in demand or supply. While change affects movement along the same curve, a shift creates a new curve either to the right or to the left indicating an increase or decrease in either demand or supply. Shift in either demand or supply occurs in situations where there is a change in the two while the price of the goods or services remains constant (Braekkan 2014, 60). Introducing technology as a means of reducing the cost of production indicates a change in production levels. Technology enables the company to produce more of the product at the same production cost. As the company delivers the products at the same value, there is no need to change the price at which an organization offers goods or services to its consumers. An increase in demand or supply while the price remains the same cause the curves to shift creating a curve indicating an increase in either demand or supply and a new equilibrium point. The new state of equilibrium will have the same price for the good or service but a different quantity.

Effect of Technology on Economy As a Whole

Examining the effect a new technology has on the economy as a whole, different aspects come into mind. One factor that has a direct impact on the economy has to do with labor. Labor and technology are two factors go hand in hand. The rational understanding that with the introduction of new technology, labor input regarding employment reduces. The phenomena are possible when examining it in the short-run. As the market introduces a new technology, the direct effect is that the innovation replaces human capital. Exploring the issue from a long-term perspective provides a different view on what technology brings to the economy.

In contrast to the short-run, in the long-run employment is created as a result of new technology. As new technology grows in popularity and new consumers continue to use the new product or service, there is the potential for new labor needed in the market (Zkexembayeva 2014). The increase in employment stems from the rise in the demand of any given product. As more people and consumers see the need of using the product, jobs are created to meet the increasing demand for the product. Employment and labor can vary from any given standpoint that includes manufacturers of the product or the necessary personnel needed to deliver the goods to the final consumer. Taking an example of the introduction of machines in factories, the immediate outcome of the new equipment will be some employees will have to be replaced by the machine. The replacement occurs because the machine can perform several duties at a go and can do the work of several individuals using less time. As time goes by, there will be the need of an individual with the knowledge and the required skill on how to operate the given machine. From the growing need creates new opportunities in the form of employment. The long-term demand for new employment opportunities as a result of new technology occurs in any industry in which consumers rely on the latest information technology. Given the growing need of employment in the long-run, the circular flow of income model is another way of illustrating the effect of technology on the economy.

The circular flow of income represents how different agents in an economy interact and exchange vital factors between the agents. From Daraban point of view, "The circular flow of income diagram is a simplified representation of the functioning of a free-market economic system. It illustrates how businesses interact with the other economic participants within the key macroeconomic markets that coordinate the flow of income through the national economy (2010, 274)." Among the exchanges that take place include factors of production such as labor, goods, and services as well as money. Any new technology can affect the circular flow of income as it is one of the factors of production. On a normal circular flow, households provide factors of production to organizations in exchange of goods and services. Households, in this case, represent potential customers of buyers who consume certain goods and services. The introduction of a new technology indicates new and improved ways of doing business as well as improving the effectiveness and efficiency of any business process. The improvement of business processes results in the production of more goods and services for the consumers to use. Below is a graphical representation of a two-sector economy.

The effect of new technology can be examined from a different point of view. Since individuals provide labor to firms in exchange of income, introducing a new technology may reduce the level of labor from individuals to firms. The reduction in labor means that the amount of income paid out to individuals also reduces. Given that the income is paid out to employees in the form of salaries, the organization will spend less on wages, and salaries expenditure paid out to individuals. Despite the effect that new technology has on the circular flow of income in any economy, new technologies can improve the current status of the economy.

An overall analysis of the economy some years back and what it has become today, it can be concluded that new forms of technology have led to the improvement of the economy. Nearly every sector of the economy feels the impact that technological innovations have to offer. The kind of product and services available today are not the same as the same as the goods and services in the market like ten years ago. Among the sectors of the economy that enjoy the effect of the new technology include the health sector, education, and entertainment (Bernstein & Raman 2015). An example of the health sector where innovations have led to the discovery of new drugs and treatment procedures that assists in improving people lives. Such medication and procedures did not exist some years back. The entertainment industry too has had its fair share of technological improvements over the past years. There has been the production of products that incorporate new and improved features. New technology can affect production levels in an economy.

Examining the production level by the use of a production possibility frontier, it is clear that new technology will determine the change in production levels. A production possibility frontier is a curve that represents different combinations of goods and services that an economy can produce at any time utilizing fully all the resources needed. According to Mert, "Economic growth occurs when an economy's production at the full employment level increases (2018)." An outward shift in the production possibility frontier (PPF) curve indicates an increase in production in any economy. The introduction of new technology into the marketplace causes an increase in the levels of production. The increase is due to the possibility of new ways of producing goods which are more accessible and affordable. As the production levels increases, there is an outward shift of the PPF curve. As a result of the outward shift, there are new combinations of the goods and services produced at different levels. In addition to indicating the various combination of production at different levels, using the PPF curve suggests that the economy is performing well as a result of the introduction of the new technology. However, the PPF curve has certain assumptions when using it to analyze economic growth. One assumption is that the economy produces only one or two types of goods. Another assumption made is that the input resources to the economy remain the same at all times which is difficult to achieve. The last assumption involves the efficient use of resources. Some of the assumptions are difficult in a typical case but still can be a possibility.

Conclusion

In conclusion, innovations have resulted in the rise in the use of technology in different sectors of the economy. New technology in any industry has its impact both in the equilibrium state of the market as well as the economy as a whole regarding the market equilibrium, new technology in most results in a shift in the demand and supply curve forming a new equilibrium point in the ma...

Cite this page

Effect of Technology on Market Equilibrium and Economy Paper Example. (2022, Nov 18). Retrieved from https://proessays.net/essays/effect-of-technology-on-market-equilibrium-and-economy-paper-example

so we do not vouch for their quality

If you are the original author of this essay and no longer wish to have it published on the ProEssays website, please click below to request its removal:

- Government Resolution to Market Failure Considering Core Values of Community and Dignity

- A Case Study of Zimbabwe's Gross Domestic Product

- Do Cell Phones Cause Cancer?

- Essay Sample on Macro-Economics: Unemployment

- Real Unemployment in Michigan Report

- Macroeconomics: Assessing Economies, Principles for Achieving Economic Goals - Essay Sample

- Paper Example on Amazon.com: Global Giant in Retail E-commerce, CSR Commitment Questioned