Accounting for a business is the fundamental activity in the determination of a firms financial position (Elliot & Elliot, 2007). All financial transactions of the business should be recorded in the journal entries and more specifically outlined in financial reports. A T-account is one of the simplest tools used to visualize accounts in the general ledger. Usually, T- accounts have double entries: debit on the left side and credit on the right side. The concept of double entry is common in modern bookkeeping (Fulks & Stanton, 2004). Double entry means that any record on the debit side must be reflected on the credit. The importance of double entry is to balance the accounts and match the relationship between assets, equity, and liabilities. Since assets are a combination of liabilities and equity, cash flows must reflect the change in income and inventory account.

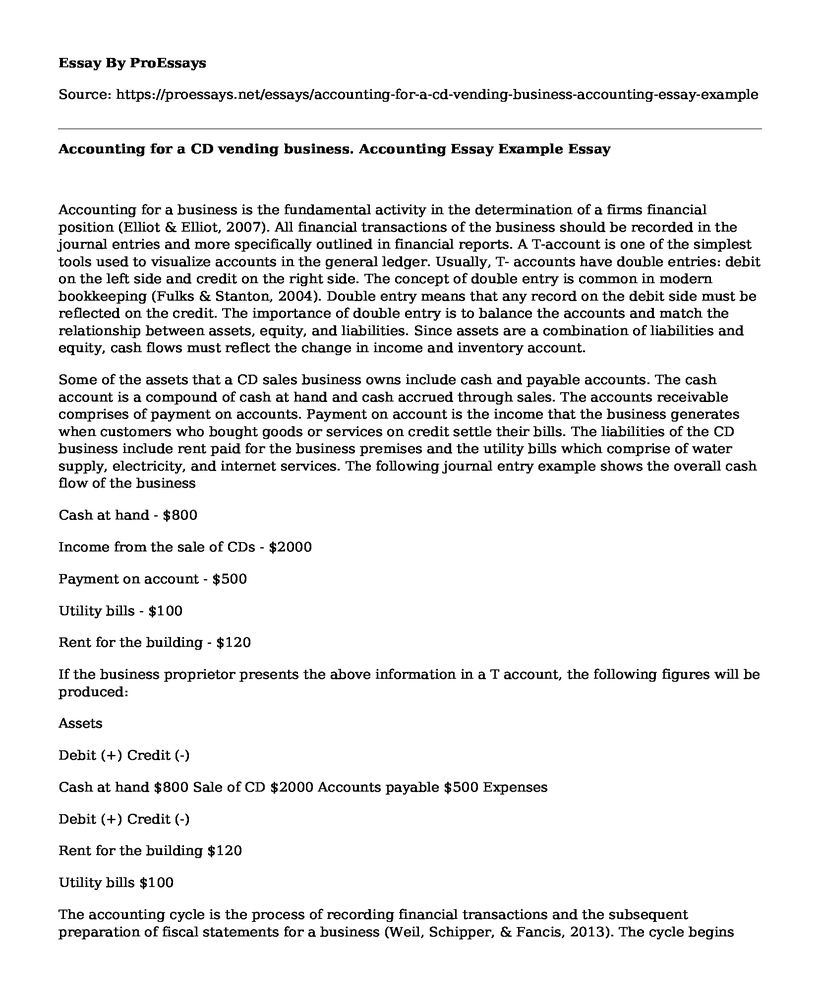

Some of the assets that a CD sales business owns include cash and payable accounts. The cash account is a compound of cash at hand and cash accrued through sales. The accounts receivable comprises of payment on accounts. Payment on account is the income that the business generates when customers who bought goods or services on credit settle their bills. The liabilities of the CD business include rent paid for the business premises and the utility bills which comprise of water supply, electricity, and internet services. The following journal entry example shows the overall cash flow of the business

Cash at hand - $800

Income from the sale of CDs - $2000

Payment on account - $500

Utility bills - $100

Rent for the building - $120

If the business proprietor presents the above information in a T account, the following figures will be produced:

Assets

Debit (+) Credit (-)

Cash at hand $800 Sale of CD $2000 Accounts payable $500 Expenses

Debit (+) Credit (-)

Rent for the building $120

Utility bills $100

The accounting cycle is the process of recording financial transactions and the subsequent preparation of fiscal statements for a business (Weil, Schipper, & Fancis, 2013). The cycle begins when the raw data is entered in the journal and ends with the final preparation of detailed statements. For the present case, each sale of CDs and payment made on account is entered into the journal. Moreover, all utility bills and rent paid are also entered accordingly. It is important to provide the date for each journal entry. The entries are consolidated and classified to end up with one figure representing each set of entries. After all the individual transaction records are made, they are compiled into an unadjusted trial balance to give a general overview of credits and debits. The last step in the cycle is to convert the unadjusted trial balance into an adjusted trial balance and the preparation of the T-accounts (Weil, Schipper, & Fancis, 2013).

In conclusion, the practice of financial accounting is an important ingredient for the success of the business. Regardless of the business size, it is crucial for the manager to keep track of the financial flows for the purpose of planning. The accounting cycle should begin with the raw entry of each transaction that leads to the exchange of money between the business and a second party. A CD business T-account shows that the business is in a financially good shape since the assets override the expenses by a big margin.

References

Elliott, B., & Elliott, J. (2007). Financial accounting and reporting. Edinburg Gate: Pearson Education.

Fulks, D. L., & Staton, M. K. (2004). Bookkeeping and Accounting. New York: McGraw Hill.

Weil, R. L., Schipper, K., & Francis, J. (2013). Financial accounting: An introduction to concepts, methods and uses. Washington, DC: Cengage Learning.

Cite this page

Accounting for a CD vending business. Accounting Essay Example. (2021, Mar 31). Retrieved from https://proessays.net/essays/accounting-for-a-cd-vending-business-accounting-essay-example

so we do not vouch for their quality

If you are the original author of this essay and no longer wish to have it published on the ProEssays website, please click below to request its removal:

- International vs. U.S. Standards

- Article Analysis: The Creation of Entrepreneurship Opportunities for People Who Are at the Base of the Economic Pyramid

- Contract Cost Analysis and Business Competencies Paper Example

- Essay Sample on International Business: Regional Economic Integration

- Ethics: The Key to a Successful Business - Lockheed Corporation Example - Essay Sample

- Report Example on International Business: Intangible Assets & Cost

- Essay Sample on FASB: Establishing Uniform Accounting Standards Since the 1920s