After her election as the president of the Kansas based Circular Club of Auburn, Shelly Jones proposed the sponsorship of a professional rodeo. The fundraiser was made an annual event with the goal of continuously growing and giving back to the community to increase its presence. In the first year of the project, the objective is to make the rodeo an annual event and break even. It is believed that the event would be able to raise five thousand dollars the following year and twenty thousand dollars in subsequent years.

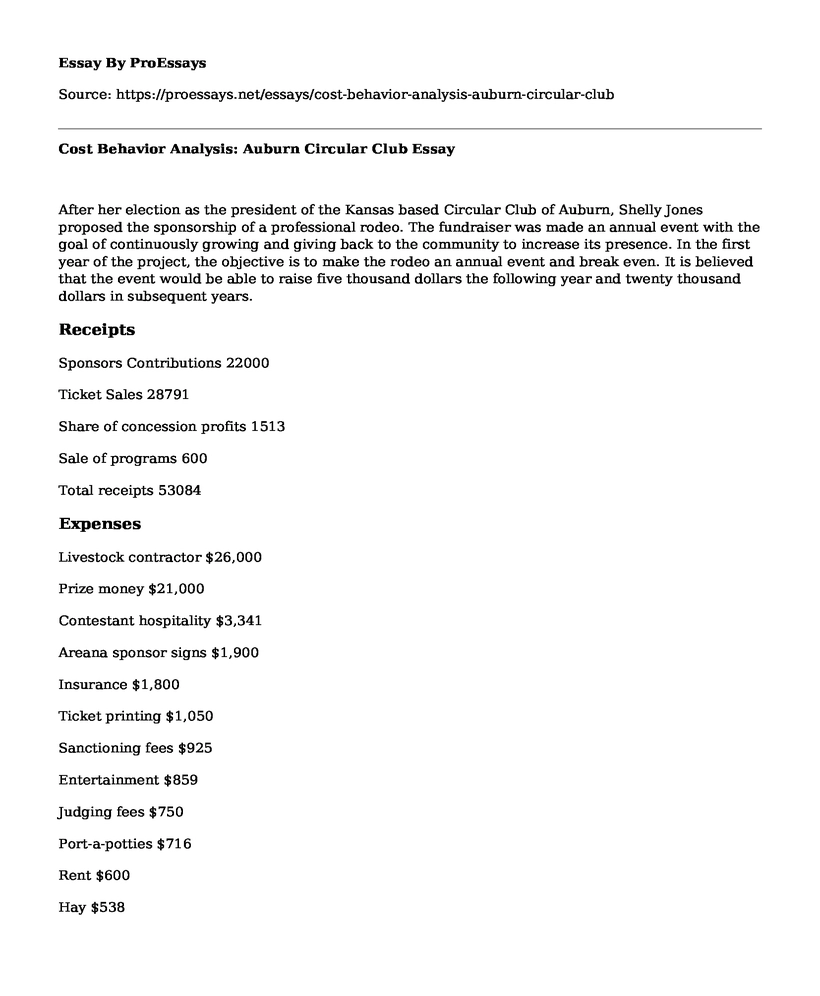

Receipts

Sponsors Contributions 22000

Ticket Sales 28791

Share of concession profits 1513

Sale of programs 600

Total receipts 53084

Expenses

Livestock contractor $26,000

Prize money $21,000

Contestant hospitality $3,341

Areana sponsor signs $1,900

Insurance $1,800

Ticket printing $1,050

Sanctioning fees $925

Entertainment $859

Judging fees $750

Port-a-potties $716

Rent $600

Hay $538

Programs $500

500 Western Hats $450

Hotel rooms $325

Utilities $300

Sand $251

Miscellaneous fixed costs $105

Total expenses $61,410

Breakeven Point = Variable Cost / Contribution Margin (Everingham et al., 2007)

Fixed Costs = $51,000

Variable Costs = 4% of $53,084

Variable Costs = $2,123.36

Contribution Margin = 100% - 4% = 0.96 (United States, 2014).

Therefore, breakeven point = $51,000/0.96

Breakeven Point = $53,125

To get the level of sales needed for Circular Club of Auburn to breakeven, the fund collected from sponsors is subtracted from the previous breakeven point, which was $53,125.

Breakeven Point of Ticket Sales = $53,125 - $25,600

Breakeven Point = $27,525

The breakeven point is a commonly used concept of economic and financial analysis. It is used not only by economists, but also by financial planners, and managers in the management of financial resources. Break-even point represents the sales level, either revenue or units, required to cover overall costs, which comprises of both fixed and variable costs (Everingham et al., 2007). At the breakeven point, the profit gained is zero and it is only possible to break even when the sales value is greater than the per unit variable cost. It implies that the sales value of a commodity must be high enough to meet the costs a company used in producing it. Once the sales surpass the production cost, the company can start enjoying its profits.

Breakeven parameter is used allows the members of the organization to identify the necessary outputs and set their goals towards meeting them. The value is the breakeven point is not generic and varies based on a given situation. The figure allows the organization to understand its sales targets and how it can start making profits. The benefit the contribution of each sale to the payment of variable and fixed costs is clearly depicted when computing breakeven point (the United States, 2014). When the organization cannot generate ticket sales equivalent to the breakeven point, then it will be a feasible venture. It should consider popularizing the event further within the community to generate sales significant enough to cover fixed costs. When the Club considers that such sales level is not feasible, it can consider reducing fixed costs through better management of expenses and rent reduction, among other alternatives. Similarly, the organization can lower variable costs, which can be through sourcing new suppliers for cheap direct inputs. All these alternatives can lower breakeven point and hence the Club need not issue any more tickets to meet fixed costs. The objective of the breakeven point to establish the least output that needs to be exceeded for an enterprise to generate a profit.

References

Everingham, G. K., Kleynhans, J. E., & Posthumus, L. C. (2007). Principles of GAAP. Cape Town, South Africa: Juta.

United States. (2014). U.S. Securities and Exchange Commission. Washington, D.C: U.S. Securities and Exchange Commission.

Cite this page

Cost Behavior Analysis: Auburn Circular Club. (2022, Apr 04). Retrieved from https://proessays.net/essays/cost-behavior-analysis-auburn-circular-club

so we do not vouch for their quality

If you are the original author of this essay and no longer wish to have it published on the ProEssays website, please click below to request its removal:

- Fundraising Plan for No Name Nonprofit

- The Audit Process

- Banks' Techniques of Data Mining Essay

- Economic Situation of Netflix Company Paper Example

- Beyond Meat Social Audit Paper Example

- Essay Sample on Cryptocurrency: Digital Asset Revolutionizing Financial Transactions

- Paper Example on Flat Tax: A System of Equality, Disadvantages, and Advantages